That gorgeous apartment building you’re buying, how is the roof? When will the HVAC units die? Did you put dollars away to be able to pay for it? And what else could fail?

These questions can nearly always be answered. No, you can’t plan for storm or fire damage but that’s what insurance is for. Big assets like roofs, though, you can and absolutely have to plan for and there are straightforward ways to do that. Let’s think about how this is done.

Are you buying an apartment building, or already own one? If you already own one and it’s small and you have deep pockets, you’re probably in good shape. You just pay up each time to replace whatever wore out. But real estate investors do their best to plan and anticipate issues. Regardless of what stage you are in your apartment investing path, follow these simple guidelines.

First, capital improvements are different from capital repairs. When you replace an asset that already exists on your property, that is a capital repair that you should be funding as “Replacement Reserves”. When you’re putting in a pool or replacing laminate countertops with quartz countertops, that is a capital improvement that you are funding as “Capital Improvement”.

Inventory the assets on the property that could wear out. Water heaters: what’s their lifespan, what’s their age, and what condition are they in today – all of them. HVAC: same questions, and are they indoors or outdoors. Roofs: again, same question, when were they last replaced, how many years are left.

Estimating their expected life span is very difficult, because it depends on a lot of factors. An outdoor HVAC unit in rainy Seattle or snowy Cleveland could rust out faster than in dry Arizona. Find out the lifespans of these assets from reputable contractors in your area. Have your roofs inspected by professional roofing specialists. Many property inspectors don’t inspect roofs or estimate remaining life. Be sure your inspector is qualified, and pay them for this service.

Then do some simple math to determine how much money you have to put away to be prepared for replacing these assets. Do you have 50 water heaters, with 10 needing to be replaced in the next year, 20 have 5 years left, and the remaining 20 have at least 10 years? Assuming you’re holding your property for 7 years and the cost of replacement is $1,000 (no, that probably isn’t the actual cost, but just for illustration), you’ll need $10,000 this year and $20,000 in 5 years. And HVAC, 50 units, 5 will die in 2 years, 25 will die in 4 years, and they cost $4,000. That means you need $20,000 in 2 years and $100,000 in 4 years. Now you add up those costs and easily see what you need each year to cover them.

![]()

Here is what you need to save:

| Year 1: | Year 1 cost + 1/2 of year 2 cost + 1/3 of year 3 cost + 1/4 of year 4 cost + 1/5 of year 5 cost = $44,000. |

| Year 2: | 1/2 of year 2 cost + 1/3 of year 3 cost + 1/4 of year 4 cost + 1/5 of year 5 cost = $34,000. |

| Year 3: | 1/3 of year 3 cost + 1/4 of year 4 cost + 1/5 of year 5 cost = $24,000. |

| Year 4: | 1/4 of year 4 cost + 1/5 of year 5 cost = $24,000. |

| Year 5: | 1/5 of year 5 cost = $24,000. |

Simple? Yes except that now you have to do this for a few more assets. It can be time consuming to gather this information and estimate it but it is necessary.

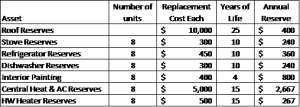

Here’s an example for a building with 8 units:

Keep in mind that you need to include replacement reserves in your underwriting. If the seller’s repair costs were nice and low, don’t get lured into thinking yours will be too. You might have a lot of old fridges, stoves, etc. that need to be replaced soon.